If you rewind the clock to February of this year, Deel, a startup that helps customers hire in other countries, announced that it had built the ability to pay workers in crypto. Regardless of your view on the financial intelligence of such a move, TechCrunch covered the news because we’re keeping tabs on Deel.

Why? Because the former startup has posted rapid historical growth, with CEO Alex Bouaziz sharing in December 2021 that it had scaled to $50 million in self-described annual recurring revenue, or ARR. The executive’s tweet indicated that Deel had started the year with around $4 million worth of ARR.

Recall that the company raised $425 million at a $5.5 billion valuation last October.

Flash forward to today: Deel shared that it crossed the $100 million ARR threshold, a key moment for any technology upstart as it implies that it has reached public-market scale — and is therefore no longer a startup by any meaning of the word.

Deel’s data point regarding its historical growth comes on the heels of Firstbase, a startup that helps companies procure and provide hardware and other remote-work needs to far-flung employees, raising $50 million after posting something like 16x revenue growth since last April.

Supporting remote workers is big business, it appears.

To dive into the Deel news, TechCrunch took a scratch at the company’s pricing page to better understand its revenue milestone and asked the company a few clarifying questions. Answers were a bit vague, but we can get a little work done. Let’s talk the deal with Deel.

Deel’s revenue growth

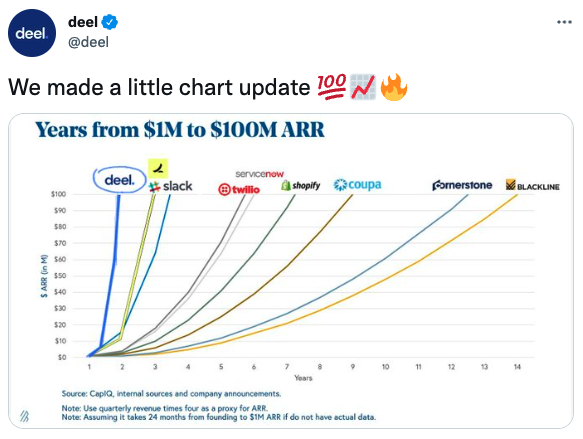

One way that startups like to brag is to take the Bessemer chart showing historical examples of startups rapidly scaling to $100 million in ARR over a short time frame. Here’s how Deel shared its own new milestone:

Image Credits: Deel Twitter

That got us curious.

To understand the revenue number, we have to understand how Deel prices its services. It generates revenue in two main ways: charging $49 per month per external contractor that it manages for a customer, or $599 per month per employee that it supports. As you can imagine, $599 per month scales nicely; to reach $100 million worth of ARR, the company would only have to manage around 14,000 workers.

Our hunch that the company was abusing the term ARR wound up being wrong. Asking on Twitter whether the company had SaaS-like gross margins (say, high 60% to mid-80% range). The CEO responded that it did. And in a follow-up email, Deel said that its “gross margins are slightly above SaaS range.”

From a gross margin perspective, then, the company’s revenue fits into the ARR rubric neatly. Deel also shared that its ARR is calculated as the “annualized value of [its] contractor and employee subscriptions,” which seems fair. Sadly, the company declined to share information on its gross margin forecasts — we’re always curious if a company’s revenue quality is improving or not — and its revenue mix.

The provided reason for not sharing those metrics was rapid growth, which is somewhat reasonable; a quickly growing company might see its revenue makeup shift back and forth from one quarter to the next. If one of its revenue sources was lower margin and going gangbusters, it could lead to gross margin erosion in the near term that the company would not want to discuss.

We’d still rather know, but also understand why Deel might want to keep potential near-term margin gyrations close to its chest. (And if its gross margins were improving, it would essentially be inviting more competition to its space if it shared that fact, right?)

Finally, Deel told TechCrunch that it’s keeping a “close eye” on its spending. We clarified with Deel that it was referring to its own spend, and not that of customers, which it confirmed. This is about as non-GAAP a profit metric as you can get, but Deel is implying that its pace of cash consumption is not terrible. We’ll learn more when we see the S-1, but for now, we can infer that the company’s losses are perhaps more derived from share-based compensation than pure cash incineration.

After poking a little at the company’s shared metric, its ARR seems about as solid as we can tell without an income statement and historical cash flow data.

That means that Deel is currently valued at a roughly 55x revenue multiple, given its prior $5.5 billion valuation. If it can double this year, that multiple will come down to something near a sane level. Perhaps Deel will manage the peak-2021 raise and valuation bump without stumbling. But given that this performance feels like an outlier, I imagine it won’t have much company if it manages to do so.